Dealing with logs and zeros in regression models

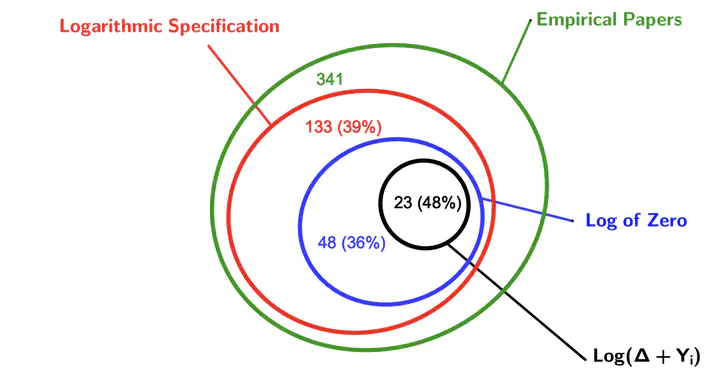

Prevalence of the Log of Zero in the AER (2016-2020)

Prevalence of the Log of Zero in the AER (2016-2020)

Abstract

Log-linear models are prevalent in empirical research. Yet, how to handle zeros in the dependent variable has remained obscure. This article clarifies this issue and develops a new family of estimators, called iterated Ordinary Least Squares (iOLS), which offers multiple advantages to address the log of zero and embeds Poisson regression as a special case. We extend it to the endogenous regressors setting (i2SLS) and address common issues like the inclusion of many fixed-effects. In addition, we develop specification tests to help researchers select between alternative estimators. Finally, our methods are illustrated through numerical simulations and replications of recent publications.

Type

Publication

Working Paper (New version soon)